BY

|

Bucket Company: How You Can Save $1000s in Tax With This Strategy

A bucket company, also known as corporate beneficiaries or a dumping company, are an incredibly useful strategy for tax planning and minimisation if done correctly suited for the right situation.

This is because it can help you “cap” the amount of tax you pay at 30% (or 27.5% for small business entities) by moving as much business income as possible through a corporate beneficiary.

As an individual or sole trader, all taxable income is assessed on a personal level and therefore, you could be liable for paying up to 45% of your income in tax, not to mention the 2% medicare levy!

In this guide, I’m going to show you how you can take advantage of bucket companies structure to help legally reduce the amount of tax you pay.

Important: Before reading on, this article has been written for informative purposes and should be used simply as guidance. Speak to a qualified accountant or lawyer if you believe the bucket company strategy is right for you.

What is a Bucket Company?

Definition and purpose of a bucket company

A bucket company, also known as a corporate beneficiary, is a strategic tool used in tax planning to distribute profits at a lower corporate tax rate rather than higher individual tax rates. The primary purpose of a bucket company is to minimise tax liability and maximise the distribution of profits to chosen beneficiaries

By leveraging the corporate tax rate, which is generally lower than individual marginal tax rates, business owners can effectively reduce their overall tax burden. Additionally, a bucket company can provide an extra layer of asset protection, ensuring that profits are safeguarded from personal liabilities.

This strategy particularly benefits business owners looking to optimise their tax position and protect their wealth.

Who is a bucket company strategy most suitable for?

This is generally best suited to investors or business owners and/or are receiving income through a discretionary trust structure.

Many business owners or investors tend to use a bucket company strategy when they have earned beyond the needs of their (and their family’s) general cost of living, which needs to be distributed somewhere at a low tax rate.

This is why it is an incredibly useful strategy for families who wish to build a wealth portfolio to potentially fund their retirement or is great for handling fluctuations in income year on year.

How can a bucket company provide tax benefits to corporate beneficiaries?

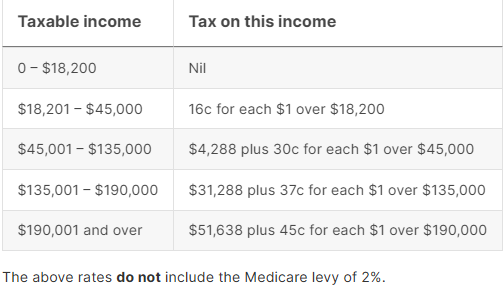

To understand the benefits of a bucket company, it’s handy first to understand the current individual tax rates. The below rates are for the 2024-25 financial year:

It is important to note that both individual and company beneficiaries pay tax on their respective portions of the trust’s income, with company beneficiaries often benefiting from lower tax rates.

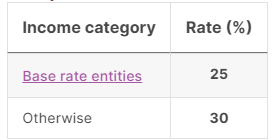

Below are the company tax rates as of 2024-25 fiscal year:

If you and your family members have used up your marginal tax rates and your income is moving into the tax rate territory above 30%, then this is when a bucket company will provide you with enormous savings.

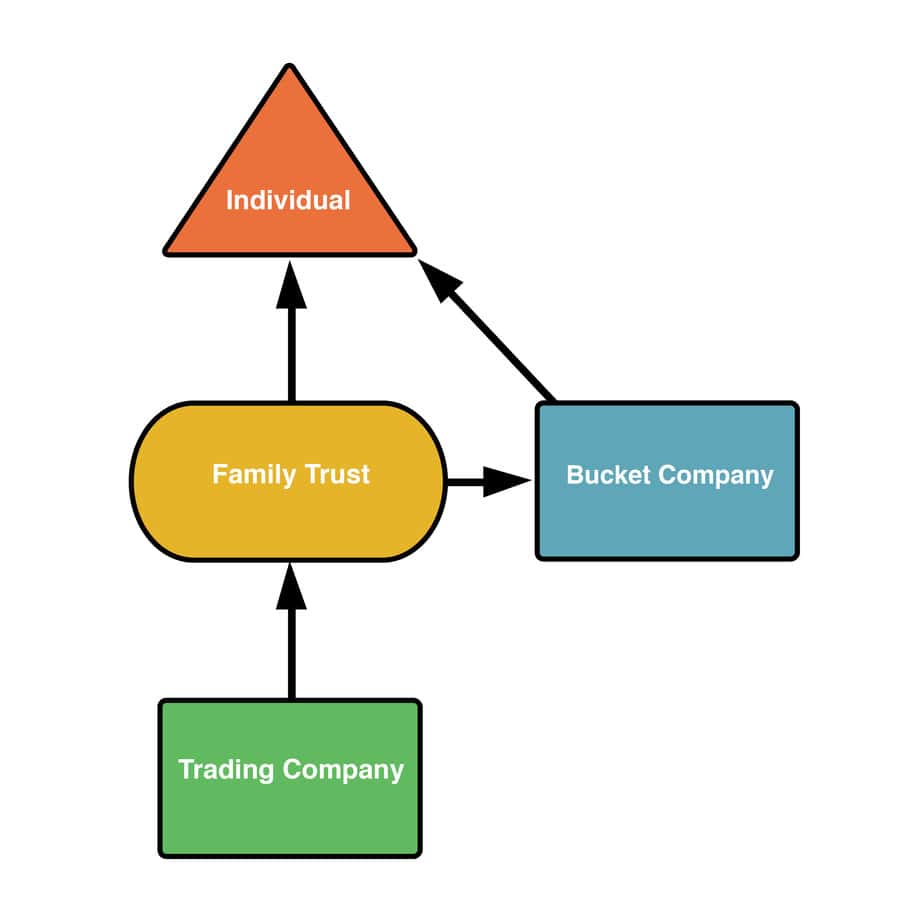

The below diagram illustrates the flow of retained profits.

How does the bucket company strategy work?

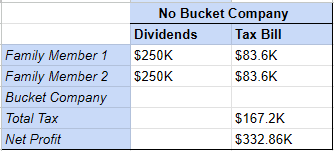

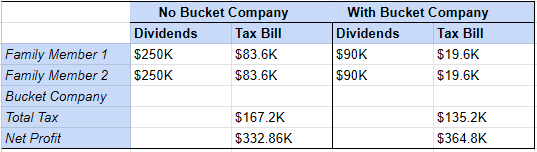

The best way to demonstrate the benefits of a bucket company strategy is to use an example, particularly focusing on the company tax rate. Let’s take a simple $500k profit as a case study.

If you’ve got a discretionary trust with $500k in profit, this income will need to be allocated to individuals or entities. In a scenario without a bucket company, this is what it would look like:

As you can see, the total tax paid is $171.2k, with net income being $328.8k.

Then, how about the bucket company strategy?

That’s a massive saving! So, can you leave the profits in the company rather than pay a dividend to the individuals?

In short – yes, you can. However, this means that the company will have retained earnings, which can expose it to risks. In situations where the company may have legal action taken against it, the claimant can go after all retained profits of the company from previous years. This is why it’s best to distribute the earnings from time to time. This is to prevent exposure and risk.

BUT.. (there’s always a but)

Setting Up a Bucket Company

Requirements and process

Setting up a bucket company involves several key steps and requirements. First and foremost, it is essential to consult with a qualified accountant or lawyer to determine if a bucket company is suitable for your specific financial situation. Once suitability is confirmed, the next step is to define the purpose of the bucket company and identify the types of assets it will hold.

The company must then be registered with the Australian Securities and Investments Commission (ASIC), which involves choosing a company name, appointing directors, and completing the necessary registration forms. After registration, a bank account must be opened in the company’s name to manage its financial transactions.

Subsequently, assets can be transferred to the bucket company, and a dividend distribution plan should be established to outline how profits will be distributed to beneficiaries. This plan ensures that the distribution process is clear and compliant with relevant regulations. By following these steps, business owners can set up a bucket company that effectively manages and distributes profits while minimising tax liability.

Do you need to pay the cash to the company?

In short – yes.

Because of the enormous potential tax savings that this strategy can afford you, you can imagine that the ATO isn’t fond of this. If cash payments are not made, this can raise Division 7A loan issues and is a big no-no for the ATO as they do not like distributions with no intention of paying them. Failure to comply with the Income Tax Assessment Act 1936, particularly Division 7A, can result in significant penalties.

Then, how can you get the cash out of the bucket company?

There are two options:

- Loan the money from the company, aka Division 7A loans; or

- Pay dividends to the shareholders of the company

Alternatively, retained earnings can be used to establish an investment company, which can hold long-term investments and generate additional income.

Let’s go into detail about this…

1. A loan from the bucket company

Some factors usually need to be considered for Division 7A loans:

- Establishing the interest rate for the repayments – these are typically set by the ATO known as benchmark interest rates. As of 2019, this is 5.2% and will increase to 5.37% in 2020

- Unsecured loans must be repaid within seven years

- Secured loans with an asset will afford you 30 years

It is also essential to establish a minimum annual repayment plan to ensure compliance with Division 7A loan requirements.

This can be handy for 20% deposits for property investments at a low rate rather than waiting to save for it before purchasing.

However, be very careful in using this option as this can be a minefield that results in legality issues if not correctly executed. Working with an accountant who knows what they’re doing with Division 7A loans will ensure that it’s being completed appropriately.

2. Dividends paid to the shareholders of a bucket company

This is a viable option, but there are a couple of things that need to be considered when paying dividends:

- Shareholders are taxed for the dividend income they receive on an individual level. However, they will receive a franking credit for the tax the company has already paid. This impact on the tax they need to be paid will need to be carefully considered

- Dividends can only be distributed according to the % of ownership in the company that they have. This means very little flexibility, and if shareholders are earning an income outside of the company, then tax minimisation can be difficult to control

BUT, There’s a THIRD Option!

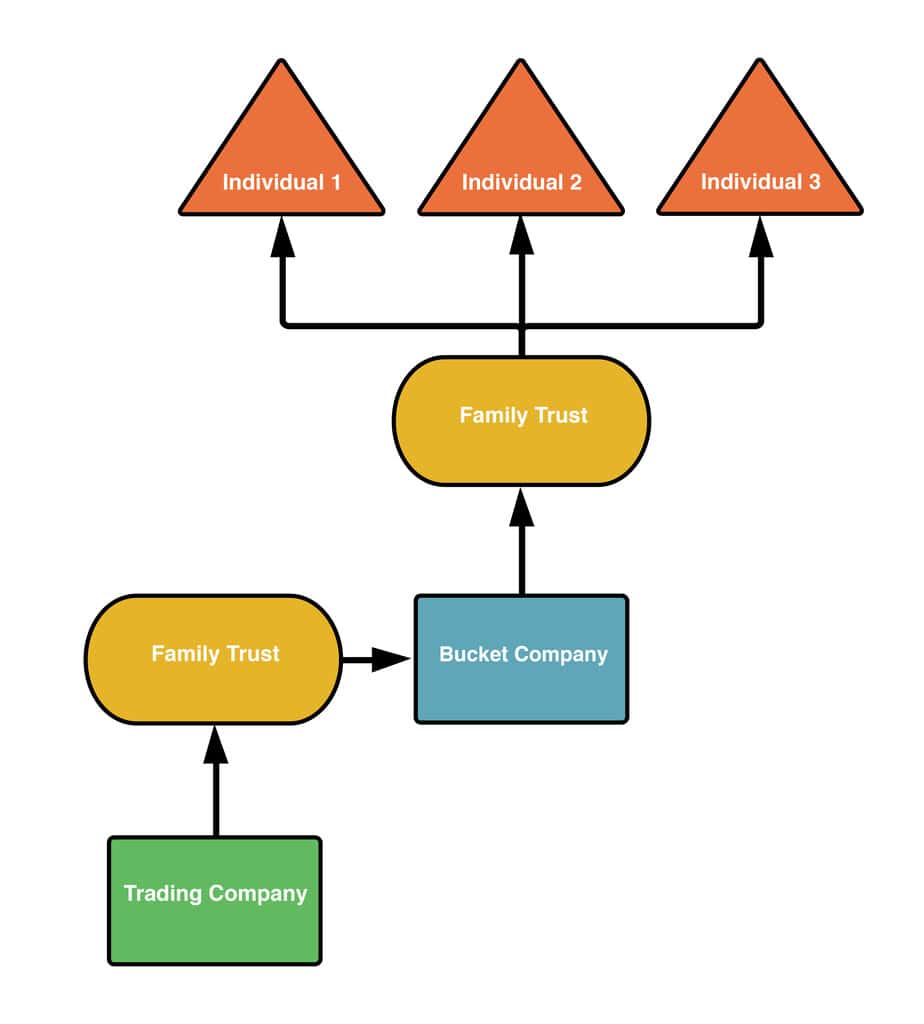

You can create a separate discretionary trust to receive the dividends from the bucket company, which can provide you with maximum flexibility on the distribution of profits in the most tax-effective manner.

This way, the new trust can be distributed according to the trust deed rather than a fixed percentage or via a loan that will incur interest.

The diagram below illustrates the exact flow of retained profits and where they end up (the individual beneficiaries).

Pros & Cons of a Bucket Company and the company tax rate

This all sounds amazing, but the ATO doesn’t want to make it too easy. Below is a list of pros and cons for a bucket company:

Pros:

- Provide another layer of asset protection

- Caps tax to a maximum of 27.6 – 30% on earnings from assets held under the company resulting in overall tax savings for the group

- Allows the business to effectively distribute the profits to entities and individuals within the family group

- Can minimise the need to pay wages and salaries to family members of the small business. This can increase costs associated with workers’ compensation, superannuation and income taxes

- Provides flexibility and some protection in investing profits of the business in other ventures such as property, shares, lending or other investments.

Cons:

- Dividends paid to individuals mean that tax is not necessarily capped at 30%

- If an individual has shares in the bucket company, this subjects them to asset risk in the case of being sued

- The 50% capital gains discount does not apply for assets held for more than 12 months by the bucket company

- Banks can charge higher rates for loans if the company wishes to borrow funds to buy assets

- Can be costly to set up and run

- Personal services income (PSI) rules may limit the ability to use a bucket company for tax minimisation.

Challenges and Considerations

Potential issues and limitations

While a bucket company can offer significant tax benefits, there are several challenges and limitations to consider. One of the primary concerns is the compliance and reporting requirements imposed by the Australian Taxation Office (ATO). The ATO closely monitors bucket companies to ensure that they are not being used solely for tax avoidance purposes.

Additionally, bucket companies may be subject to additional regulations and oversight from other government agencies, which can increase administrative burdens. The company’s tax rate may also be influenced by its status as a base rate entity, affecting the overall tax benefits.

Furthermore, the distribution of dividends from the bucket company to individual beneficiaries can be subject to personal income tax, potentially reducing the overall tax savings. It is crucial to carefully consider these factors and seek professional advice to navigate the complexities and ensure compliance with all legal requirements. By doing so, business owners can maximise the benefits of a bucket company while mitigating potential risks.

What should I invest in? Should the individual or the company invest with the funds?

The answer to this is – it depends on what you wish to invest in and the financial situation of all involved.

The tax payable on investments will vary depending on whether the individual or the company holds the assets.

Considerations that come into play here include the 50% capital gains discount that does not apply to companies; the amount of tax liability of each individual; what are the borrowing capabilities of the company and the individuals (and which one is better for purchasing assets), among a plethora of other variables.

As you can see, there isn’t a simple solution to this.

This sounds complicated. Do I need a bucket company?

Everyone’s situation is different due to multiple factors that can come into play when considering whether this strategy is right for you.

This strategy may not be for everyone given that it’s a very technical method of tax planning and minimisation with a range of potential pitfalls.

You’re subjecting yourself to high running costs, and you’ll need to ensure you’re following the law.

So, it’s almost always recommended that you engage a qualified accountant or lawyer who has experience in bucket companies to take a look at your situation.

You can book in a free initial 45-minute consultation with one of our Chartered Accountants to assess your situation to decide whether a bucket company strategy is suitable for you.

Sign up to our monthly newsletter where we share exclusive small business and contractor advice!

Disclaimer:

Please note that every effort has been made to ensure that the information provided in this guide is accurate. You should note, however, that the information is intended as a guide only, providing an overview of general information available to contractors and small businesses. This guide is not intended to be an exhaustive source of information and should not be seen to constitute legal or tax advice. You should, where necessary, seek your own advice for any legal or tax issues raised in your business affairs.