BY

|

What is a Family Trust? The Essential Guide

Family trust benefits can have significant positive impacts on your family group finances for some individual situations.

In the most recent study on trusts by RMIT University, it was reported that there were nearly 850,000 trusts during the 2015 – 16 financial year in Australia – that’s one trust for every 29 people at the time. The cumulative value of the assets totalled $3 trillion.

The same report estimates that between $672 million to $1.2 billion of tax revenue is being sheltered annually using trusts.

So why are so many Australians using family trusts and what benefits can they afford your family group?

In this guide, we’ll explain why so many Australians are using family trusts and what benefits (and disadvantages) of having a family trust are.

What Is a Family Trust?

A family trust is a discretionary trust set up to manage a family group business or hold a family’s personal or business assets.

A family trust is discretionary in nature because the trustee can independently exercise their decision making. In other words, the trustee can exercise their discretion when it comes to the distribution of income and capital among the beneficiaries.

There are several reasons for setting up a family trust. The most common include:

- for property investment;

- for a family business investment;

- asset protection; and

- to manage family income.

How Does a Family Trust Work?

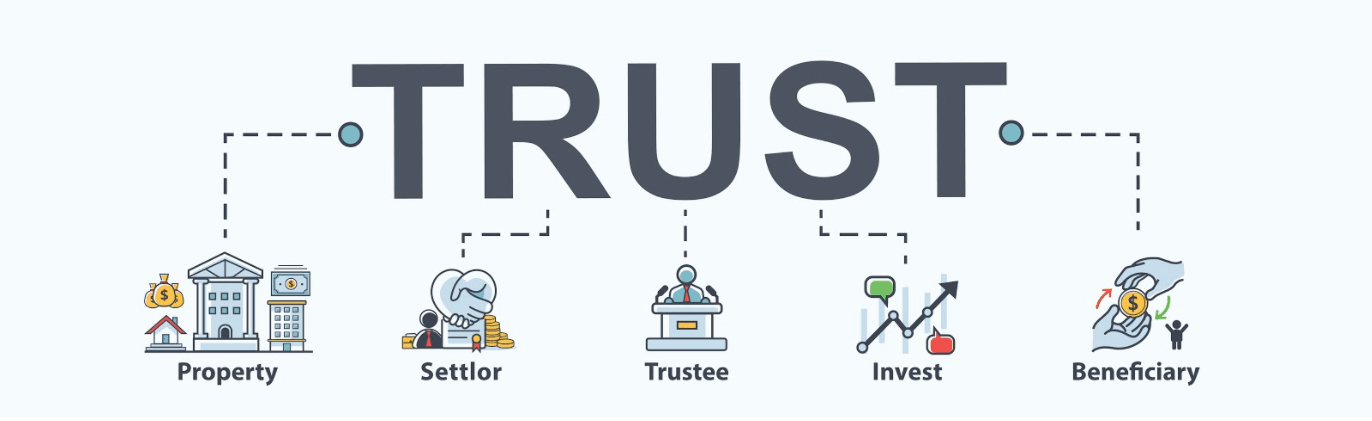

Setting it up involves a family trust election and an agreement where one party holds assets to the benefit of other parties. There are several critical components need to be featured in the family trust election:

A. The Settlor

The settlor is the person responsible for establishing the family trust as well as naming the trustee and the beneficiaries.

Once the settlor has put the trustee in charge of the trust property and defined which persons are considered beneficiaries; the trustee is required to agree to act in terms of the agreement.

At this point, the family trust is established, and the settlor will have no further role in connection with the trust or its property.

The settlor can be a close friend, an accountant or a lawyer. For tax purposes, however, the settlor should not be a beneficiary of the family trust.

B. The Trust Deed

The trust deed is the legal agreement that will prescribe how the family trust will operate and the role of each of its parties.

You can think of this document as the “terms and conditions” of the family trust.

C. The Trustee

The trustee of the is the individual or corporate entity who is responsible for:

- the family assets within the trust; and

- for ensuring that the trust is managed per the trust deed.

The trustee similarly holds the authority to distribute any income and capital gains of the trust to the nominated beneficiary, at its full discretion.

It’s important to note that under trust law, trustees are personally liable for the debts of the trust they administer.

D. Who Can Be a Beneficiary of a Family Trust?

As the name suggests, beneficiaries are some individuals or companies who benefit from family trusts.

Beneficiaries have no control over the family trust. Instead, the trustee will nominate which beneficiaries are entitled to receive income or capital gains from the trust in a given financial year.

Generally, family trusts have primary beneficiaries with all the other beneficiaries defined by their relationship to the primary beneficiaries.

You can, similarly, nominate “unnamed” beneficiaries to include the extended family of the primary beneficiaries. For example, if you would like to have your child’s future husband/wife and their children, you can include them in the trust as unnamed beneficiaries.

How to Set Up a Family Trust

Before setting up a family trust, it’s highly recommended that you consult with a financial professional to get appropriate financial advice for your specific circumstances and objectives for the trust.

However, the process is briefly outlined below:

- Step 1: Select your trustee

- Step 2: Draft the trust deed

- Step 3: Appoint a settlor to sign the trust deed and hand over the initial settlement sum to the trustee

- Step 4: The trust beneficiaries and trustee(s) will gather for a meeting in which the trust deed is formally accepted, and the trustee(s) agree to be bound by the terms outlined in the deed

- Step 5: Lodge your trust deed with the relevant revenue authority and pay stamp duty (if applicable in your state)

- Step 6: Apply for both an Australian Business Number (ABN) and a Tax File Number (TFN) for the trust.

- Step 7: Finally, a bank account should be opened for the trust.

How Much Does It Cost To Set Up a Family Trust?

When setting up a family trust, you’ll be required to cover the cost of:

- creating the trust deed document;

- consultation fees with a financial advisor to get financial advice on who to nominate as a trustee, for example;

- initial settlement fees;

- stamp duty (if applicable);

- registration of its TFN with the Australian Tax Office; and

- registration of an ABN with the Australian Business Register.

So, the initial setup fee could cost you around $2,500.

Benefits of a Family Trust

Provided that the family trust is executed in the right way, it can provide significant benefits.

1. Asset Protection

In most cases, family trusts are useful when it comes to protecting assets from bankruptcy or business failure.

As the assets in the trust belong to the trustee, they can’t be used to pay creditors of the individual beneficiaries.

Thus, if you hold your assets within the trust rather than under your name, the property cannot be used to settle the debt owed.

2. Effective Tax Planning

A trustee can make income allocations based on the distinct tax circumstances of each family group member.

For example, if the trust has beneficiaries who have a lower marginal tax rate, the trustee can distribute more income to them so that they pay tax at a lower rate.

By splitting the income tax allocation, the trustee can effectively minimise the general tax obligations of the family members who benefit from the trust.

Additionally, there are tax benefits should the trustee use the family trusts to acquire investment properties, for example.

Provided that the investment property is held in the trust for more than twelve months, the trust will be eligible for a 50% capital gains tax discount, upon its eventual sale.

3. Flexibility To Distribute Income

As the trustee can exercise its discretion when it comes to the distribution of income and capital among the family group beneficiaries, family trusts can be beneficial for protecting vulnerable family members who may make rash spending decisions.

A trustee could prevent a beneficiary who has a gambling addiction, for example, from accessing a large capital amount that could be quickly and poorly spent.

Many families also use family trusts as a method for succession planning by giving access to more capital when children become older. This could help support their studies, for example.

Disadvantages of a Family Trust

Establishing a family trust is not without certain risks:

- Loss of ownership of assets: you will have to transfer ownership of your assets to the trustee, who will become the new legal owner.

- Ongoing management: you’ll need to consider the cost involved in meeting the trust’s administrative requirements such as annual bookkeeping and accounting.

- Undistributed income earned by the trust could be taxed at a high marginal tax rate.

- Distributions to minors are taxed up to 66%.

- In some states, owning properties through a family trust means that your property may not be eligible for the tax-free land threshold.

Key Takeaways

There is no “one size fits all” when it comes to family trusts.

While there are significant benefits to establishing a family trust, including tax benefits and flexible wealth distribution, these benefits are entirely dependent on your family’s specific circumstances.

At Box Advisory Services, our small team of experienced accountants can help you navigate through the decision of opening a family trust and give you the financial advice you need before establishing the trust.

To find out how we can help you, book in a free consultation with us to assess your situation.

Sign up to our monthly newsletter where we share exclusive small business and contractor advice!

Disclaimer:

Please note that every effort has been made to ensure that the information provided in this guide is accurate. You should note, however, that the information is intended as a guide only, providing an overview of general information available to contractors and small businesses. This guide is not intended to be an exhaustive source of information and should not be seen to constitute legal or tax advice. You should, where necessary, seek a second professional opinion for any legal or tax issues raised in your business affairs.